LSA will be making revisions to some of the Mutual Fund, ETF, VUL, and a select number of VA portfolios in the coming days. Below is a schedule of when the revisions will be posted to the LSA website.

With regard to the portfolios not listed below, we will announce that schedule next week on Wednesday June 12th, 2013.

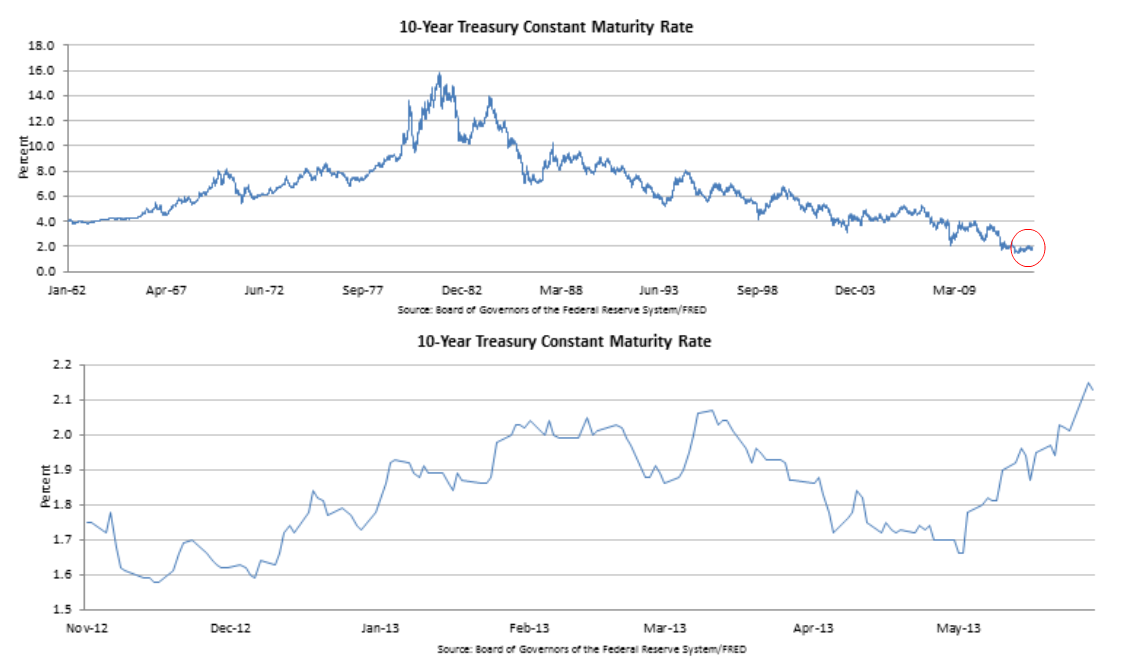

Although we do not believe this is the big shakeout in bonds that has been predicted when rates start to increase it is a precursor of what is to come when the Fed cuts QE3 & starts to increase interest rates.

The big issue moving forward is where to go with these low risk bonds that we are targeting to replace. We will be focused on alternative solutions such as: Market Neutral, Commodities (which also had a difficult May), Unconstrained bonds, & Multi-Alternative investments.

As always, the rationale and explanation for the changes, as well as all new fund fact sheets can be found on the LSA website under “Portfolio Management” as they are posted.

Here is the schedule of release dates. Please login to the LSA site to view all changes:

Thursday June 6th, 2013:

- ING Golden Select VA

- ING Select Advantage

- ING VUL

Friday June 7th, 2013:

- JNL Elite Access

- JNL VA

Monday June 7th, 2013:

- Lincoln VA

- Nationwide VA

- ETF Tactical Allocator

- ETF Income First

- ETF 7 Model Series

- PC Blended

Tuesday June 11th, 2013:

- SBL Advisor Deisgn

- SBL Secure Design

Wednesday June 12th, 2013:

- Prudential

- Prudential w/ Rider

Video commentary discussing the changes will be posted over the next few days. LSA will be e-mailing out a link to the replay. If you have any questions please feel free to contact us at support@lsaportfolios.com or call us at (866) 581-5724.