Labor Markets

(+) The initial jobless claims number after seasonal adjustment was 340,000 in the week ending May 18, slightly lower than the expected 345,000. Filing for first-time unemployment insurance benefits fell by 31,000 compared to the same time last year. The 4-week moving average of initial claims was 339,500 versus 370,250 in 2012.

(+) Continuing claims for the week ending May 11 fell to 2,912,000, better than the median forecasted 3,000,000. The figure was 3,296,000 in the comparable week in 2012. For the year-to-date, continuing claims have shrunk by 217,000.

Housing Markets

(+/0) April existing-home sales rose 0.6% to a seasonally adjusted annual rate of 4.97 million, according to the National Association of Realtors. It is slightly below the expected 4.98 million-unit level. April’s resale activity is 9.7% higher than the 4.53 million-unit level in April 2012. Low inventory, tight credit, and 31% more buyer traffic are pushing the national median existing-home price up 11% from April 2012. The median time on market for all homes was 46 days in April, compared to 83 days in April last year.

(+) Federal Housing Finance Agency’s Housing Price Index (HPI) shows the Q1 U.S. house prices increased 1.9% from 4Q12. Compared to 1Q12, house prices rose 6.7%. The upward price momentum occurred across all regions of the country. The purchase-only HPI index for March 2013 stood roughly the same as the November 2004 index level.

(+) New-home sales for April increased 2.3% month-over-month at a seasonally adjusted annual rate of 454,000, slightly faster than an expected 425,000. New-home sales rose the most in the West by 10.8% but declined the most in the Northeast by 16.7% in April. The monthly supply of new homes on the market is 4.1 months, tighter than 4.9 months from a year ago.

Manufacturing Economy

(0) Data for April manufactured durable goods report is mixed. New orders were up 3.3% in April from the prior month to $222.6 billion, reversed from March’s 5.9% decline. It was a positive surprise compared to a median forecasted 1.6% increase. The higher new orders came from broad-based industries, but primarily driven by defense aircraft and civilian aircraft orders. Excluding transportation, new orders still rose 1.3%, ahead of an expected 0.5% increase. On the negative side, shipments of capital goods (including defense and nondefense industrial equipment and parts) fell 3.3%. Defense capital goods shipments declined by 5.6%, seeing a negative impact from the federal sequester spending cuts that went in effect March 1. Nondefense capital goods excluding aircraft also decreased 1.5%, lagging the consensus -0.5% rate.

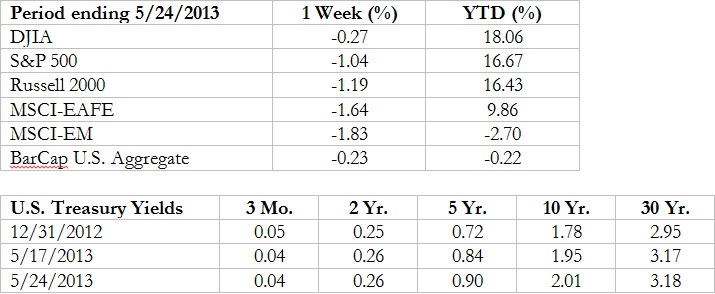

Market Notes