April’s Non-Farm Payroll report is a solid set of data that should go a long

way to correcting the unnecessary angst caused by the March report, not least

since that month’s data has now been revised up strongly from 88K to 138K in

Total Payroll and from 95K to 154K in Private Sector gains, making this in

retrospect a normal set of data. This is not the first time this cycle that we

have seen initially weak data revised strongly higher within 30 to 60 days, and

we have to assume that market participants will now start to develop a much

greater resilience to weak payroll data should it be released in future months.

As for April’s report itself, the BLS estimated gains of 165K for Total Payroll

(beating 140K consensus) and 176K for Private Sector gains (150K consensus), in

line with the trailing 12 month ma of 180.5K. It also revised higher the

already very strong February data which now shows gains of 332K Total and 319K

Private Sector gains, making this something of a “blow out” month in retrospect.

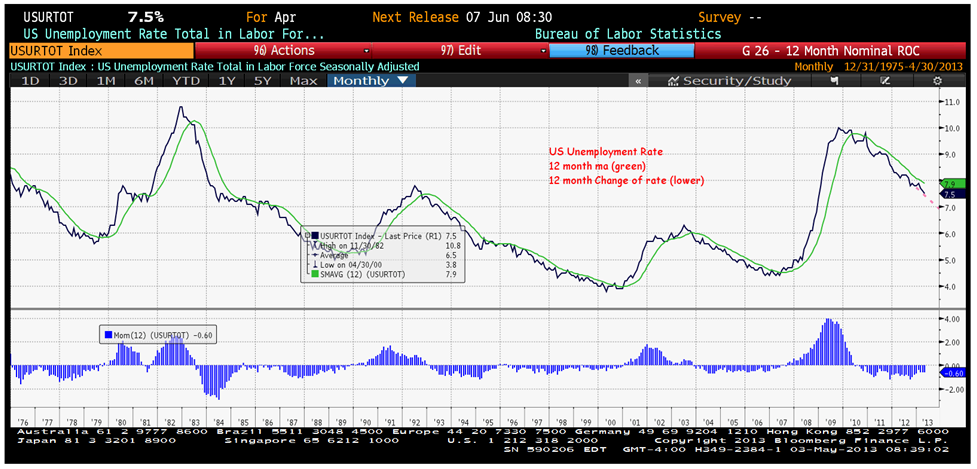

The icing on the cake was supplied by the Unemployment Rate falling to 7.5%. As

we had pointed out last month the Household Survey has been unusually poor for

several months making it highly likely that April would supply strong data.

This duly arrived in the form of a 293K monthly gain, which had a predictable

effect on the Unemployment rate. As the attached chart shows, Unemployment

remains in a well-defined declining trend which is on track to take the rate to

6.5% around this time next year, approximately 18 months ahead of the FOMC’s

tardy schedule. Perhaps a more relevant time period is Q3 2013 when the rate

may well be pushing against the 7.0% level, which we suspect would be the point

at which the bond market starts to exhibit clear concern that the FOMC has been

way behind the curve in its assumptions and actions.