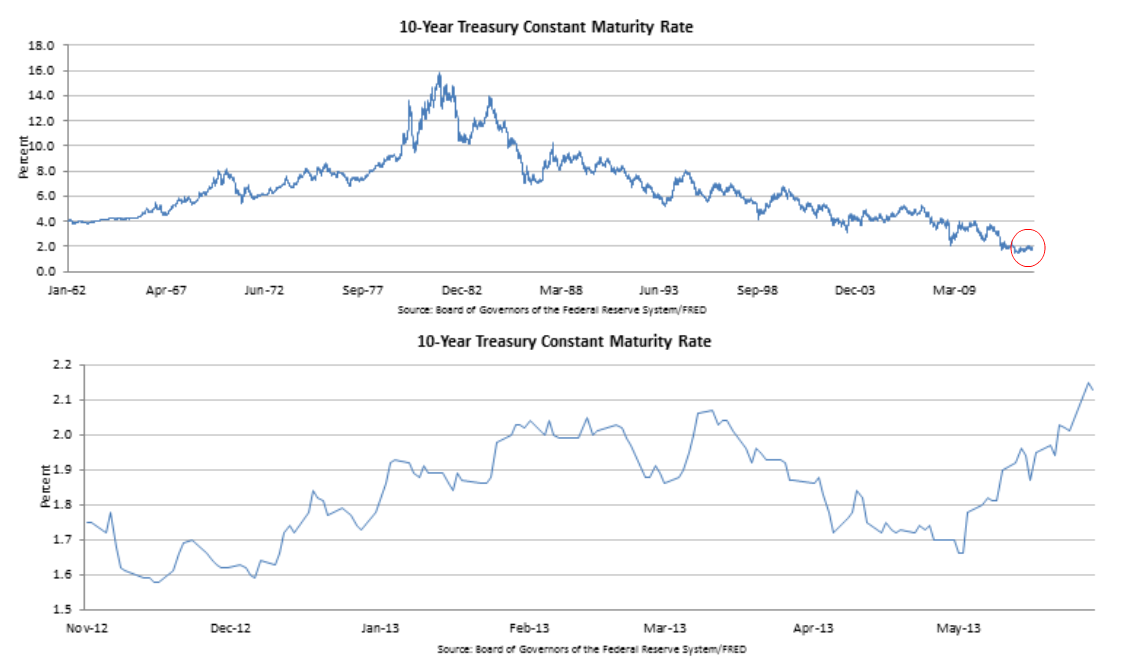

This week’s news was highlighted by the FOMC meeting, which resulted in a reiteration of the current policy of accommodative mortgage and treasury bond buying. However, further comments regarding the timing of the inevitable ‘tapering’ off of QE down the line were taken quite negatively by several asset markets—including global stocks, bonds, real estate and commodities.

One would have thought the Fed was raising rates by a few percent based on the reaction, but all Chairman Bernanke clarified in the post-statement press conference was that the Fed expected to reduce its stimulus later this year, and perhaps end bond purchases entirely by mid-2014, assuming unemployment falls in accordance with current projections (towards their target of 6.5%—which itself is subject to future adjustment). As we mentioned in the special Fed note last week, the market reaction was somewhat ironic in that the eventual exit was taken as a short-term negative (markets falling several percent with Treasury yields rising), while it actually signifies a greater degree of confidence in the recovery and a lessened need for government stimulus.

With a dearth of other world crises to worry about last week, perhaps Fed policy is being even more closely scrutinized than normal. Nothing concrete was said in regard to current bond-buying or interest rate strategy specifically; rather, it was a bit of additional clarification on timing of potential activity if current trends continue—trends that many well-regarded economists have been forecasting and commenting on for some time (in fact, many feel the Fed is being overly optimistic in their timelines). We wish we could say (not really) that some new and surprising development was shared that underpinned this negative reaction. But it wasn’t. This potential exit plan has been analyzed and modeled over and over again for several years now by both those inside and outside the Fed, and will continue to be going forward—if not more so. More below on how this relates to portfolios. Continue reading