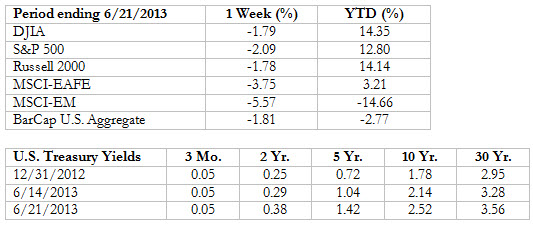

This week’s news was highlighted by the FOMC meeting, which resulted in a reiteration of the current policy of accommodative mortgage and treasury bond buying. However, further comments regarding the timing of the inevitable ‘tapering’ off of QE down the line were taken quite negatively by several asset markets—including global stocks, bonds, real estate and commodities.

One would have thought the Fed was raising rates by a few percent based on the reaction, but all Chairman Bernanke clarified in the post-statement press conference was that the Fed expected to reduce its stimulus later this year, and perhaps end bond purchases entirely by mid-2014, assuming unemployment falls in accordance with current projections (towards their target of 6.5%—which itself is subject to future adjustment). As we mentioned in the special Fed note last week, the market reaction was somewhat ironic in that the eventual exit was taken as a short-term negative (markets falling several percent with Treasury yields rising), while it actually signifies a greater degree of confidence in the recovery and a lessened need for government stimulus.

With a dearth of other world crises to worry about last week, perhaps Fed policy is being even more closely scrutinized than normal. Nothing concrete was said in regard to current bond-buying or interest rate strategy specifically; rather, it was a bit of additional clarification on timing of potential activity if current trends continue—trends that many well-regarded economists have been forecasting and commenting on for some time (in fact, many feel the Fed is being overly optimistic in their timelines). We wish we could say (not really) that some new and surprising development was shared that underpinned this negative reaction. But it wasn’t. This potential exit plan has been analyzed and modeled over and over again for several years now by both those inside and outside the Fed, and will continue to be going forward—if not more so. More below on how this relates to portfolios.

(0) The consumer price index rose +0.1% for May, while the core CPI gained +0.17%—both below the forecasted +0.2% for each segment. During the month, energy prices rose nearly one-half percent, while apparel, transportation services and owners’ equivalent rent also gained a few tenths of a percent each. On a rolling twelve-month basis, headline and core inflation rose +1.4% and +1.7%, respectively, implying that food/energy prices rose at a slower rate than the basket of other items (specifically, natural gas utility and restaurant prices explained a bulk of the increase). In looking at alternative inflation measures created by the Atlanta and Cleveland Fed branches over the past year, ‘sticky’ CPI (consisting of prices for goods that don’t change frequently, like housing and household furnishings) rose +2.0%, while the ‘flexible’ CPI (prices of goods that do change quite frequently, including fuel prices, autos and hotel rooms) rose only +0.1% for the trailing period.

(+) In real estate, existing home sales rose +4.2% for May, which outperformed the forecasted +0.6% gain. An increase in single-family home sales of +5% was responsible, while multi-family/condos fell by -2%. Regionally, the Midwest experienced the sharpest improvements (+8%), although all parts of the country were positive in the magnitude of 2-4%. These results brought the year-over-year existing home sales gain to +13%. The months supply of existing home inventory fell to 5.1, compared to 6.6 a year ago. Notably, sales described as ‘distressed’ (foreclosures/short sales) represented a fifth of the total, which is decline from being a quarter of all sales a year ago at this time.

(0/-) Housing starts rose +6.8% in May, which underperformed the +11.4% gain expected. Single-family starts rose a third of a percent, while multi-family starts were up +22% (recovering from April’s sharp decline, and this is a relatively inconsistent series month-to-month). For the trailing twelve month period, the total housing starts series has gained almost +30%. Building permits fell -3.1% in May, which was just a tick worse than expected. A small gain in the single-family permit series was offset by a -10% drop in the multi-family segment.

(+) The National Assoc. of Homebuilders Housing Market Index rose from 44 in May to 52 in June—surpassing expectations of a 45 reading and bringing the index to its highest level since Spring 2006, boding well for this forward-looking measure of housing start activity. In the details of the report, builder assessments of current sales, future sales and prospective buyer traffic all rose in more or less equal degrees.

(0) The general business conditions component of the New York Fed district’s Empire manufacturing survey improved dramatically to +7.8 in June from -1.4 in May, which surpassed consensus calls for a zero reading. Some underlying components in the report, though, were not quite as strong, with weaker results from new orders, shipments and employment/workweek length. Interestingly, certain regions in the district (particularly lower-lying areas near Long Island and the lower Hudson Valley) reported that the aftermath of Superstorm Sandy has adversely affected revenues for as long as seven months after the storm.

(+) Similarly, the Philadelphia Fed manufacturing index rose from -5.2 in May to +12.5 for June, compared to a forecasted -2.0 result. However, the underlying details were stronger than the New York report this week, with shipments, new orders and employment metrics all higher. Expectations for capital spending over the forward-looking six-month period were also strong. These regional reports have been mixed, but not all bad, so there could be less of a slowdown than feared this spring/summer.

(+) The Conference Board’s index of leading economic indicators increased +0.1% in May, keeping the more meaningful six-month growth rate trend intact. For the month, financial indicators (such as interest rate spread, stock prices and credit spread conditions) were the positive index contributors, while the manufacturing survey and orders data, as well as employment, detracted from the results. The coincident and lagging indicator indexes rose a similar +0.2% and +0.3%, respectively. All of these indicators continue to chug upward in a consistent trend path from their 2009 lows.

(-) Initial jobless claims for the June 15 week rose a bit higher than expected, to 354k, compared to a consensus estimate of 340k, with no special factors convoluting the series. Continuing claims for the June 8 week came in at 2,951k, which was lower than the 2,958k expected and maintained the trend of improvement this year.