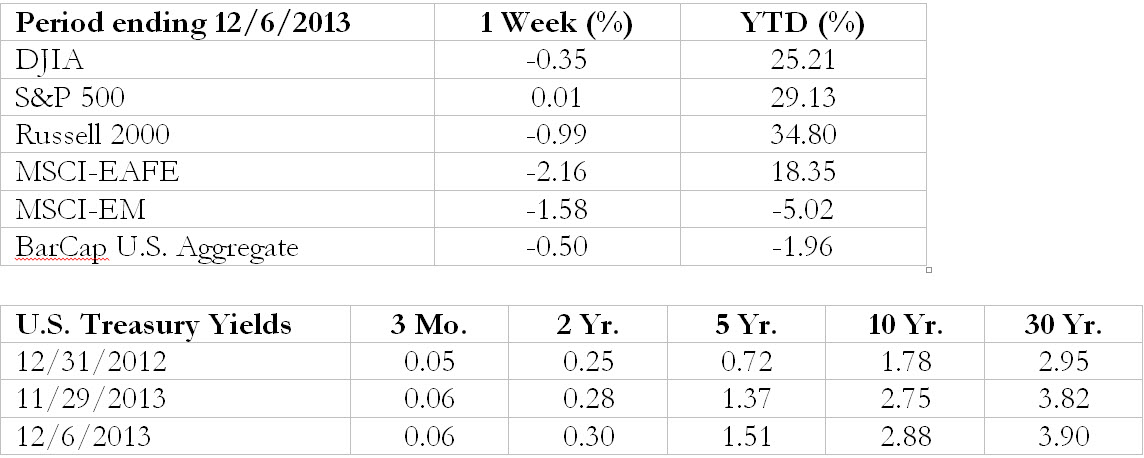

Following the holiday, it was somewhat of a big week for economic reports as we head into the final pre-Christmas stretch.

(+) The second estimate of 3rd quarter GDP was revised up substantially from the original 2.8% to 3.6%, which was about a half-percent above expectations (which obviously also called for some improvement on the original advance estimate). The positive contribution originated almost entirely from growth in inventory accumulation, though, which removes some of the luster off of the large adjustment.

The estimated GDP for the 4th quarter is hovering around 1.5-3.0% or so—about the widest variance in figures seen in some time. Likely, that means it will show up somewhere in the middle. For 2014, estimates are biased higher, in the 3.0-3.5% area as expectations for lessened fiscal drag, better consumer spending (due to lower deleveraging activity) and finally improved business capex are slated to kick in. Globally, 2014 is looking to be a much better year with expected growth moving from sub-3% to the mid- to upper-3% range, brought about by positive results in Europe, U.K. and some key members of the EM complex, not to mention the U.S.

(+) The ISM Manufacturing report came in stronger than expected—in fact, the highest since April 2011—rising from October’s 56.4 to 57.3 for November, surpassing the median forecast of 55.1. Underlying details were also stronger, with higher readings from new orders, production and employment; while inventories declined (not all bad). This report reflects a bit of mid-cycle strength, which has been a feature of the past few cycles, including 2005 and 1999.

(-) By contrast, the ISM Non-manufacturing index came in a bit weaker for November, falling from October’s 55.4 to 53.9 (expectations called for 55.0). Business activity and employment both declined by about 4 points each and new orders declined just slightly (but stayed above 50, notably).

(+) The final Markit PMI number for November rose a bit from the preliminary release, to 54.7, which slightly surpassed expectations for 54.3 and was about 3 points higher than October’s PMI. Output and new orders were strongly higher in November, while employment was just half a point weaker.

(+) The U.S. trade deficit narrowed from September to October, from a revised -$43.0 bil. to -$40.6 bil., versus a forecasted deficit of an even -$40.0 bil. The ex-petroleum balanced accounted for much of the difference (over $2 bil.). Exports have grown about 2% over the summer, surpassing import growth of almost a half-percent, which has also help shrink this difference.

(+) Motor vehicle sales for November rose more than anticipated and reached another new post-recession high point. Expected total sales of 15.8 mil. were bested by the release of 16.3 mil., and domestic sales came in at 12.6 mil., about half a million over forecast. Car sales continue to plug along quite nicely. The holiday season sales incentives are probably helping a bit as well.

(0) Factory orders for October fell -0.9% month-over-month, which was in line with the expected -1.0% decline. Core capital goods orders were revised up slightly for both Sept. and Oct., which played into the dynamics somewhat.

(+) Construction spending rose +0.8% for the month of October, surpassing the forecast of +0.4%. The government shutdown caused the Sept. number to also be released along with October’s, which offered a slight decline of -0.3% (consensus called for +0.5%), so part of this offsets, when coupled with some downward revisions for July and August. Notably, the single-family component declined for both Sept. and Oct., which hasn’t happened for two years. However, the positive news is that state/local government construction expenditures rose over +3% in the month (best since the crisis), which coincides with other data affirming local government recovery based on better tax revenues and some belt-tightening.

(+) New home sales broke out of a few disappointing summer months to an October +25% month-over-month gain (444k homes, which surpassed a consensus estimate of 429k); this offset a poor September result released at the same time due to government shutdown delays. Removing the usual monthly noise to a multi-period view, it appears data from the last three months shows increases in all four regions of the country, moving the overall picture to nearer that of summer prior to the weak patch. Inventory levels also moved a bit tighter to 4.9 months’ sales. Overall levels continue to report well below normal, to the extent that a 50% bump would need to occur for new home sales to recover to just over half of the activity seen a decade ago. We’re not building enough homes yet, but we’ll eventually need to.

(+) The Univ. of Michigan consumer sentiment index for December came in stronger than expected, at 82.5, which was an improvement from November’s 75.1 and this month’s anticipated 76.0 reading. Consumer assessments of the present situation and future expectations both improved by several points. Interestingly, the bulk of the improvement came from lower-income households, which perhaps were most discouraged during the government shutdown and have now seemingly recovered. Inflation expectations for the year ahead ticked up a tenth to the ‘normal’ 3.0%, while the 5- and 10-year look ahead expected inflation figures were just a two ticks below that at 2.8%.

This survey appears in the news frequently and we often mention the results, as it adds some behavioral color to Americans’ economic views, which can influence spending and investment behavior. But what does it really cover? It’s quite simple, actually…the five primary questions surveyors ask each month that are included in the index calculation are listed below (side note: this is more detail than anyone probably really needs or cares about, so feel free to skip over this portion if you don’t have the interest, but we think it’s informative to know where the underlying metrics for these surveys come from).

1) We are interested in how people are getting along financially these days. Would you say that you (and your family living there) are better off or worse off financially than you were a year ago?

2) Now looking ahead—do you think that a year from now you (and your family living there) will be better off financially, or worse off, or just about the same as now?

3) Now turning to business conditions in the country as a whole—do you think that during the next twelve months we’ll have good times financially, or bad times, or what?

4) Looking ahead, which would you say is more likely—that in the country as a whole we’ll have continuous good times during the next five years or so, or that we will have periods of widespread unemployment or depression, or what?

5) About the big things people buy for their homes—such as furniture, a refrigerator, stove, television, and things like that. Generally speaking, do you think now is a good or bad time for people to buy major household items?

There are a handful of other questions in addition to these, which make distinctions between today’s conditions vs. those expected down the road, for instance, as related to employment prospects, family income, interest rates, inflation, how good a job the government is doing (the Fed, by implication), housing prices/rents, gasoline prices, timing of auto purchases, amount of assets in stocks, etc., but you get the picture. They are simply and casually written, for a broad range of income audiences, in an effort to gauge the quickest and easiest-to-contemplate response from the largest number of respondents. Interestingly enough, it gives us a lot of what we need to know about sentiment, which is perhaps why it’s been in use since the early 1950’s.

(+) On to employment, the ADP report came in better than anticipated, rising by +215k in November (expectations called for +170k). Additionally, the September and October numbers were revised upward from 145k to 186k and 130k to 184k, respectively. The strongest gains have continued to come from professional/business services (a gain of almost +40k) as well as trade/transports (+45k). We always tend to mention this, but sometimes the private ADP survey has sporadic results with what the government produces a few days later; nevertheless, the additional data point is useful as a gauge of private sector activity (and all of these surveys contain flaws/biases).

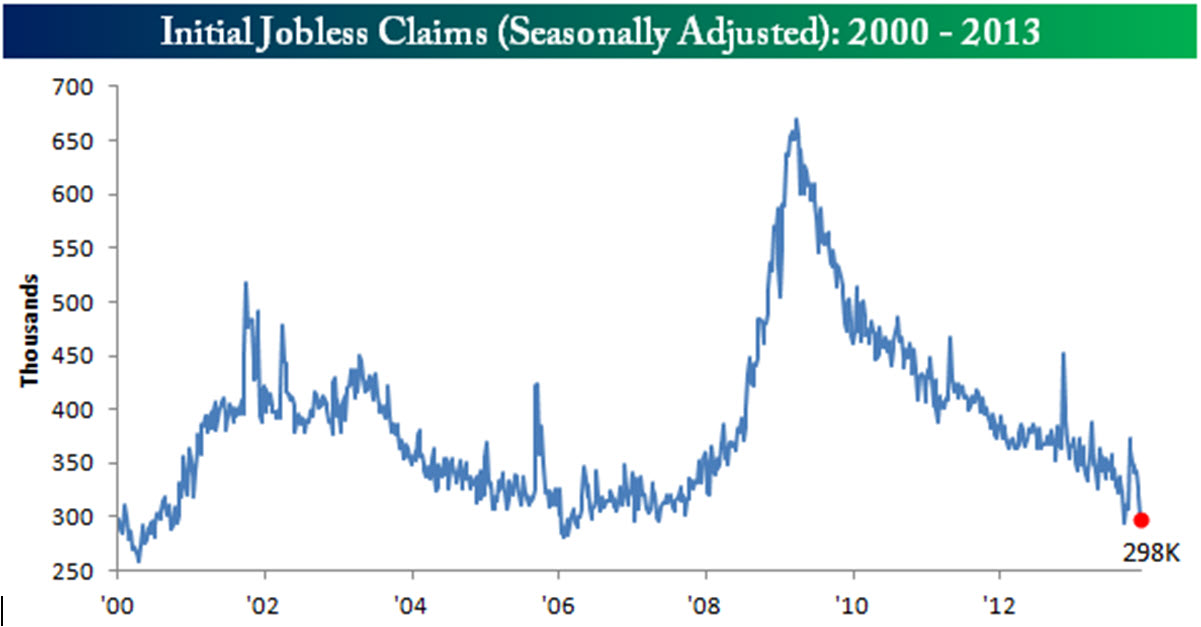

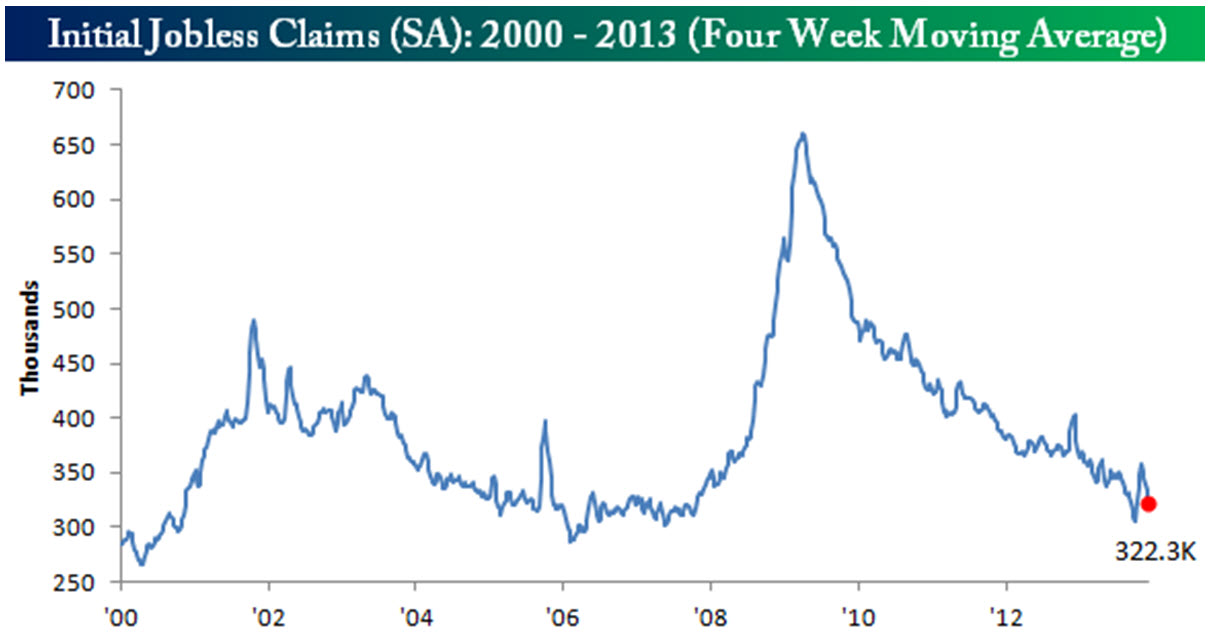

(+) Initial jobless claims for the Nov. 30 ending week fell to 298k, from a revised 321k the prior week—far better than the 320k estimate—and under 300k for only the second time during the expansion. No special events convoluted the data, but the Labor Dept. noted that seasonal adjustments around the holidays can be a challenge. Continuing claims for the Nov. 23 week came in at 2,744k, lower than the 2,800k expected and about 20k lower than the prior week.

Source: Bespoke Group

The ‘big’ government report was much stronger than expected. Nonfarm payrolls for November rose +203k, which beat the forecast +185k, and surpassed the psychological 200k mark. Revisions for the prior two months amounted to a gain of +8k, which is not especially relevant statistically, but certainly not bad news. From an industry standpoint, the largest gains were in trade/transport/utilities (adding +60k jobs) and education/health services (added +40k), however, manufacturing also posted a strong +27k result. On the negative side, unsurprisingly, Federal government jobs fell by -7k, however state/local jobs rose by roughly double that amount. State and local governments, buoyed by a better economy and higher tax revenues, have been in better shape lately, which job growth reflects.

The unemployment rate fell from 7.3% to 7.0%, the lowest in five years (and better than the forecasted small improvement to 7.2%). The labor force participation rate, which has been closely watched as of late due to the questions about a smaller labor pool affecting the final rate calculation, rose a few ticks to 63.0%. However, it’s still low, and potentially problematic, as we’ve discussed in prior weeks.

In other related releases, October personal income fell -0.1%, versus an expected gain of +0.3%—contrary to the half-percent growth trend of the last few months. However, core wages and salaries grew just a tenth of a percent, which is more meaningful this month, as the headline number was affected by ‘farm’ income, which tends to be more sporadic anyway but was impacted by a Sept. class action suit payment by the USDA. Consumer spending rose a tick better than anticipated at +0.3% for the month, while the personal savings rate fell four-tenths to 4.8% of disposable income (note: consumers have been delevering, are they almost done?). Average hourly earnings rose +0.2%, on target with forecast and rolling 12-month earnings figure is +2.0% higher—right in line with other inflation calculations. The average workweek rose to 34.5 hours, as expected. The PCE price index was unchanged, but the core PCE rose 7 hundredths of a percent—close to forecast.

Markets responded positively to the monthly news, and the probabilities of the Fed taking tapering action in December rose perhaps. However, most odds remain on January or March. Criticism of the Fed for not acting sooner in light of the recent stronger data, and perhaps worrying too much about the bond market, has intensified, and these questions may continue.

(0/+) The December Fed Beige Book was released and continued on its theme of growth at a ‘modest to moderate’ pace, as has been the trend. The tone was a bit more optimistic this time, though, which was a bit of a positive change, particularly in manufacturing centers like Chicago, in the semiconductor-focused San Francisco district and aerospace in the Seattle area. Residential real estate comments were positive, but a bit less so than in past reports, in keeping with tempered outlooks for price appreciation. Consumer activity in regards to retail and auto spending were generally positive as well, albeit cautious about the holiday season. For a change, the government wasn’t specifically mentioned as a sticking point, other than the regulatory environment and concern about potential benefit cost increases from Obamacare.

In currency news, it was reported last week that the Chinese yuan overtook the euro in October to become the second-most utilized currency in trade finance. The U.S. dollar remains the primary currency of choice, at just over 81%, but the yuan’s share is now just under 9%—remarkable considering the share was only 2% two years ago—with the primary countries using it being those in the immediate area (China, Hong Kong, Singapore) but also Germany and Australia. We only mention this as a side note to give some perspective on the arguments calling for the U.S. dollar’s demise as the world’s reserve currency. Anything can happen over time, naturally (the dollar took over for the British pound around World War II). In terms of allocated reserves, the dollar also stands as the largest-owned currency, with the euro being a distant second and no others really in the running for a clear third place (Yen and Pound).