Dear,

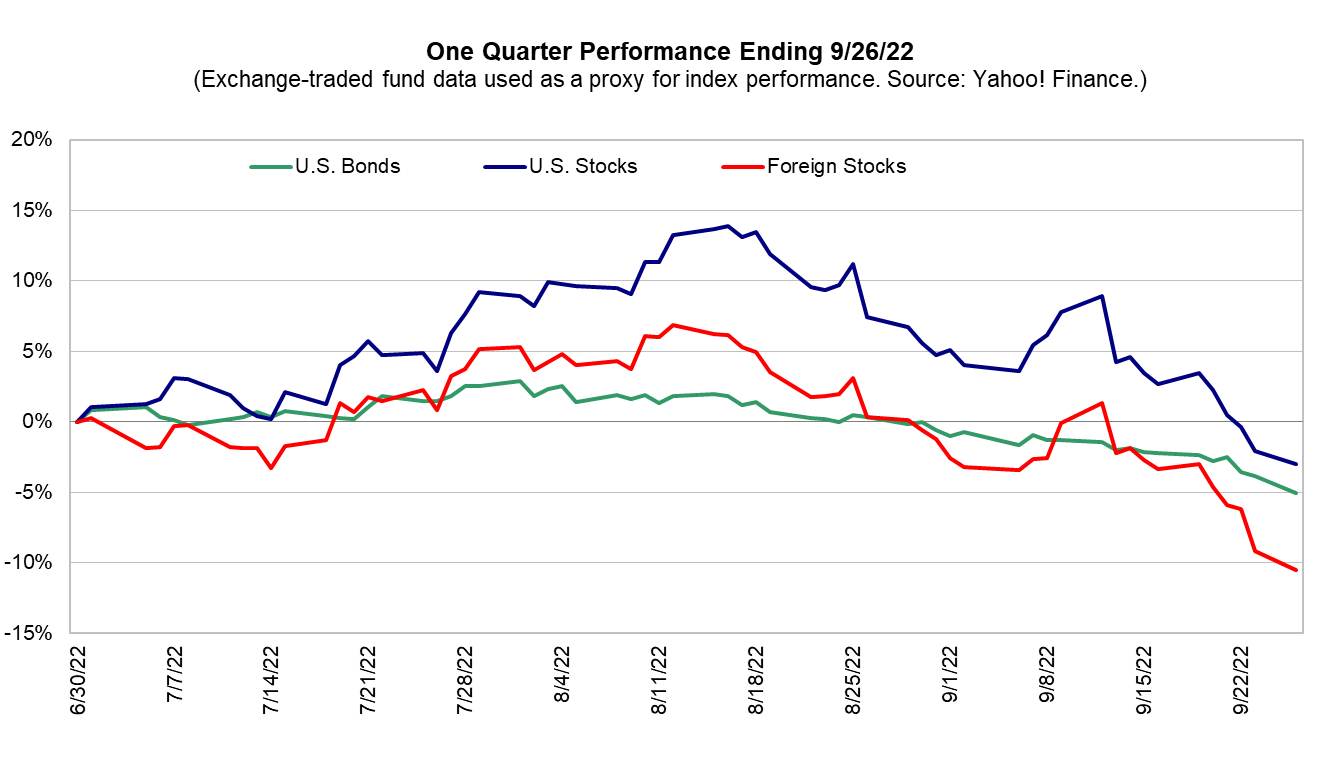

Well, gosh, here we are again. This last quarter started on a somewhat positive note with stocks rising until the middle of August. That cheer didn’t last however as uncertainties about rising interest rates and the direction of the economy pushed us back to a bit lower than where we started. Bonds followed a similar pattern as folks wrestled with the idea that interest rates would climb higher than had been anticipated earlier this year.

Predicting the future for the various markets is impossible but that doesn’t prevent the pundits from trying. We do know that this year has been full of surprises, and we wouldn’t be taken aback if there aren’t a few more before this period of volatility is done.

As always, folks’ consternation about the markets and their portfolio is in direct proportion to the timeline they are considering. If one’s focus is short term, and their measurement of success is based on several quarters of portfolio performance, these are dire times indeed. If, however, one takes a longer-term view, then the events of a particular quarter or year become less important and can be integrated with their overall financial plan.

All that said however, it is worth reviewing just what the drivers have been of this year’s volatility. The three main factors at play have been inflation, interest rates and the economy.

The inflation we’ve been seeing over the last period is, for the most part, a continuation of the disruption caused by the pandemic. The interruption of supply chains, the scope of the stimulus programs and the changing preferences of the purchasing public have caused inflation to rise dramatically. While policy makers at first thought this would self-correct in short order that hasn’t been the case.

The Federal Reserve Board, in response to changing conditions, has likewise changed their response, ratcheting up the size of the periodic interest rate increases that began early this year and signaling a potentially higher eventual interest rate plateau, the point at which further increases will no longer be necessary.

All this leads to the economy. Through much of the year the economy continued to show signs of growth despite the actions of the Fed. Leading economic indicators, as measured by the Conference Board, continued to rise through August. The last few months have seen a change as those indicators have pointed downward, increasing the probabilities that this round of interest rate increases will not result in the longed for “soft landing” but instead might finally push the economy into some level of recession.

Just how does all this play out with the capital markets? The higher levels of inflation we’ve been seeing unnerve investors because folks understand the Fed will have to continue to raise rates to push inflation back down. Rising rates, and the uncertainty of how high they will go, affect stock and bond prices. Stocks are affected because the level of short-term interest rates is an important input in the calculation of a “fair market value” (price) for stocks. Higher rates imply lower stock prices for a given level of future earnings (more on that in a moment). Bonds are affected because as rates rise bond prices must fall to make the dividend yield comparable to those same new higher rates.

Finally, the prospect of recession creates uncertainty for stocks because of the effect that recessions have on corporate earnings. If earnings fall, then the price the market is willing to pay for that declining stream of earnings is invariably less.

So, when we take all of the above, throw in a war in Europe, uncertainty about fuel and food supplies and spice with a bit of supply chain woes, a tight labor market and general election angst we have the perfect recipe for the very sour portfolio stew we’ve been served of late.

But wait, what about that long term view we mentioned earlier? Don’t the markets factor that in? Markets do look ahead, but not terribly far. Mr. Market tends to be a somewhat short-sighted and excitable fellow.

You and I, on the other hand, have the ability to look a little further out in time and are encouraged to do so because we understand that it is good for our financial health in general and our portfolio specifically. Is the potential for recession already priced into today’s market level? Will we fall into a recession caused by higher interest rates? It certainly matters over the short term but isn’t that important when we think about our portfolio over longer periods.

Our last recession was caused by the pandemic induced shut down. This one, if indeed we do fall into recession, will be a function of inflation and the higher interest needed to bring inflation down. Recessions, while painful at the time, are generally short-term while expansions are much longer-lived. The period since the last great war has been a triumph for those optimists who surmised that growth was the natural order of things and that invested in accordance with that belief.

While waiting for that bright future to unfold we’ll continue to take steps to add value to your portfolio. Market selloffs like this provide opportunities as Mr. Market’s excitable nature causes him to run away from particular sectors and asset classes or invest too heavily in others. We’ll continue to be on the lookout for areas of the stock and bond markets whose values become overly skewed to the down or upside. The value stocks introduced last year helped reduce some of the downside so far this year and the bond portion of portfolios have benefited from exposure to shorter maturities and floating rate bonds, both of which have not been as affected by interest rates.

Sooner or later the selling will stop, and the market will rebound. It is never any fun waiting for that to happen. In the meantime, diversification, coupled with a disciplined approach, continues to offer the best methodology for minimizing volatility while remaining invested in order to participate in the eventual gains of the markets and economy.

We’re happy to discuss the impact this market turmoil has on your financial plan, just let us know.

We hope the rest of this year is fruitful for you and your family and that you get to enjoy the best of what autumn has to offer.

We appreciate your trust and confidence in us and we remain,

Optimistically yours,

“ Worrying is like paying on a debt that may never come due.” – Will Rogers