Economic Update 2-20-2018

- In a busy week for economic releases, highlights included weakness in retail sales and some hints of increasing inflation as measured by import prices, PPI and CPI. On the positive side, manufacturing continues to look robust in several regional surveys and jobless claims remain very low.

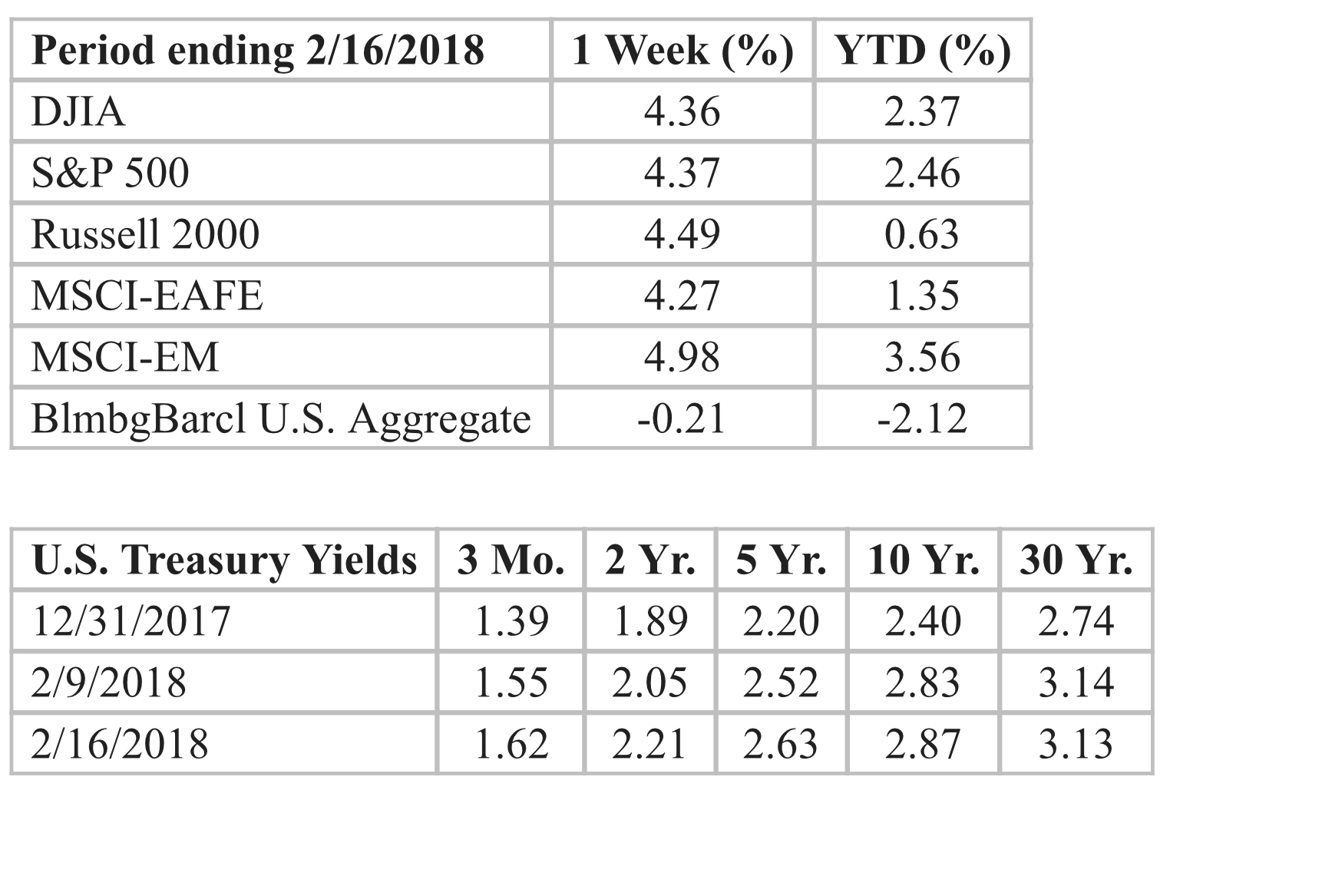

- Equity markets around the globe gained sharply on the week to rebound from their recent correction. Bonds fell back again as interest rates inched higher in reaction to higher inflation and expectations of stronger growth. Commodities regained some ground as well, led by higher crude oil prices and a weaker dollar.

U.S. stocks recovered lost ground last week as volatility returned in the positive direction—with stocks experiencing their strongest-returning week in five years. Every sector ended in the positive, with information technology and industrials gaining the most ground, while telecom and energy came in last place. The recovery appeared to be led by strong earnings and fundamentals, fewer concerns over inflation strengthening, and other news, which included details about the administration’s infrastructure plan, such as over a trillion dollars of new investment and a streamlined regulatory environment. Speaking of earnings, 80% of firms in the S&P have now reported, with the index showing a Q4 year-over-year gain of +15%. Although energy has led the way with strong year-over-year comparatives, S&P ex-energy is also up a solid +13%. Revenue gains are also up in the +10% range. Interestingly, dividend payouts are also rising.

Foreign stock returns in Europe, U.K. and Japan were also positive for the week, to a lesser degree—however, a weaker dollar pushed returns up to a level equivalent to those in the U.S. As in the previous few weeks, the primary driver of non-U.S. equity returns appeared to be market sentiment in the U.S., although fundamentals and earnings growth abroad continues to show improvement. Japanese GDP grew for the 8th consecutive quarter, albeit only at an annualized rate of +0.5%, with imports rather than exports leading the way—a shift from prior trends. In emerging markets, stronger global growth and, to some degree, commodity pricing has again boosted Brazil, China and Russia, while South Africa earned double digit returns as the problematic long-standing president finally stepped down.

U.S. bonds lost ground again as interest rates continued to move higher along with increased year-over-year inflation data and heightened expectations. High yield bonds were the best-performing segment, with indexes moving higher, while floating rate bank loans also outperformed traditional bonds, with flattish performance. Foreign bonds ended the week little changed in local terms, but a weaker dollar pushed these several percent higher for the week. Emerging market bonds fared slightly better than developed, as spreads again contracted.

Real estate gained slightly, to a lesser degree than broader equity markets. In the U.S., mortgage and timber REITs fared best, with gains more similar to other stocks, while retail/malls showed weaker gains in keeping with weaker retail sales results. Europe and Asia fared better, due to the tailwind of a weaker dollar.

Commodity indexes gained ground as the dollar fell. All segments ended the week with positive returns, led by industrial metals and energy. Crude oil recovered over the week by +4% to end at $61.55, despite reports of increased production upcoming and even fears of a glut.

Sources: LSA Portfolio Analytics, American Association for Individual Investors (AAII), Associated Press, Barclays Capital, Bloomberg, Deutsche Bank, FactSet, Financial Times, Goldman Sachs, JPMorgan Asset Management, Kiplinger’s, Marketfield Asset Management, Minyanville, Morgan Stanley, MSCI, Morningstar, Northern Trust, Oppenheimer Funds, Payden & Rygel, PIMCO, Rafferty Capital Markets, LLC, Schroder’s, Standard & Poor’s, The Conference Board, Thomson Reuters, U.S. Bureau of Economic Analysis, U.S. Federal Reserve, Wells Capital Management, Yahoo!, Zacks Investment Research. Index performance is shown as total return, which includes dividends, with the exception of MSCI-EM, which is quoted as price return/excluding dividends. Performance for the MSCI-EAFE and MSCI-EM indexes is quoted in U.S. Dollar investor terms.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product.