The first FOMC meeting of the year was uneventful, as expected, with no action on the interest rate policy front, with short-term rates kept to a targeted range of 1.25-1.50%. There were no dissents. As there was also no planned press conference, formal comments and a Q&A session from new Chair Powell will have to wait until March.

The official statement noted several items, including that the labor market has continued to strengthen, and economic activity has been rising at a solid rate. This is in addition to improvements in employment, household and business spending. However, inflation was noted as continuing to run at a sub-target pace, but some progress has been seen recently. This fairly optimistic assessment was largely taken as a sign of another interest rate hike in March, which would be in keeping with their recent pace.

As for the dashboard of relevant policy items:

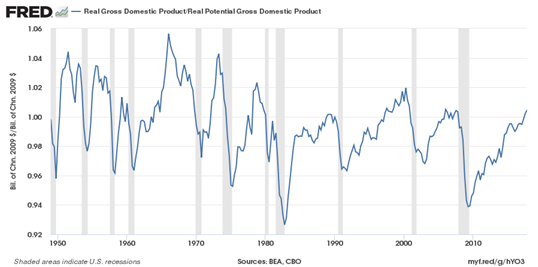

Economic growth: Growth for Q4 came in at 2.6% on a preliminary release, which is considered decent in the context of the past several years, but not as strong as the expected 3.0%, or the 3-4% growth rate touted by the administration as highly achievable over the coming year. When looking at current GDP levels relative to ‘potential GDP’—the estimated level based on a high utilization of current resources without generating inflation—we are indeed running higher. This is not uncommon for this point in the cycle (seen in the historical chart below). This excites politicians naturally, but economists realize that a growth pace that is ultimately ‘too hot’ begins to run on borrowed time and can sow the seeds of its own destruction. Tax reform added an extra boost to growth and company earnings that was taken by markets as a welcome shot in the arm, but it may not have been that badly needed, especially since we appear to be moving toward the latter innings of the current recovery business cycle anyway.

Click to enlarge

Inflation: Core CPI has been running at just under the 2% Fed target, while headline inflation, with the wavering influence of energy price changes, has been a few ticks higher on a year-over-year basis. With price levels/inflation being one component of the Federal Reserve’s mandate, current readings would argue for a relatively neutral policy stance, with pressures not underwhelming or overwhelming. Debate continues here, too, about the practical definition the Fed’s ‘target’—as to whether it should be an overly-specific (or even rules-based) quantitative goal or merely refer to a long-term trendline where minor deviations above and below are to be expected.

Employment: Labor conditions, the other key component of the Fed’s mandate, are running hot. We’ve spoken before about the theoretical level of ‘full’ employment, which is generally accepted as the point of sustainable minimum unemployment levels, given demographics and the small group outside of the employable universe. After falling below this level and headed perhaps into the 3’s in 2018, thoughts could turn to how long this labor winning streak can last and what a pullback might eventually look like. At that time, such as year-over-year deceleration in employment, recession odds will no doubt move higher, per history.

Current consensus thinking on the more conservative side is pointing to about two rate increases in 2018, spaced out to June and December, while the Fed itself has anticipated three, and more aggressive ‘bulls’ are assuming four this year. Of course, this all depends on the continued robustness of the economic expansion, and the accompanying pick-up in inflation that is generally expected to coexist (although we’ve been waiting some time for this). There are peripheral issues in the bond market as well, including the gradual balance sheet run-off of U.S. treasury holdings, which adds to supply, as will deficit spending to finance the recent tax cut. Thus far, any supply issues that would have resulted in higher interest rates have been tempered to some degree, with rate increases coming as a reaction to stronger economic growth; however, signs of inflation or a weakening of foreign demand for treasury debt are feared as rate catalysts. Bond yields are unpredictable, prone to changes in near-term news, and thus very difficult to forecast, so all must be taken with a grain of salt. The inflation that would send rates soaring that has been predicted for years has been persistently absent, and the unique demand from foreign buyers has been exceptionally strong (when competing rates for high-quality debt in locations such as Japan and Germany are far lower).

On the investment market side, the flatter yield curve has been one of the more discussed treasury market dynamics of the past few months. However, as long-term yields drive higher, actually steepening the curve and alleviating these concerns, other worries about the effects of rising interest rates surface. Higher rates can be a byproduct of stronger economic growth, but there is a balance—rates deemed ‘too high’ can be the trigger of the avalanche by suppressing growth. Naturally, when the Fed raises rates to put the brakes on activity, this is exactly the point—essentially removing the ‘punchbowl’ as the party is getting going. Markets just don’t want the Fed to be too quick or too good at the task. For now, however, overall conditions remain quite solid. Earnings growth has been an overwhelmingly important driver for equity returns over time, with conditions here remaining positive, with foreign prospects continuing to look even more interesting than domestic.