In fear of the inevitable raises of the federal funds rate, many investors are beginning to speculate whether or not fixed income still has a place in their portfolio. With us being about a decade removed since the last time we saw a rate hike, it may be hard to remember that we have been through such periods of rising rates before.

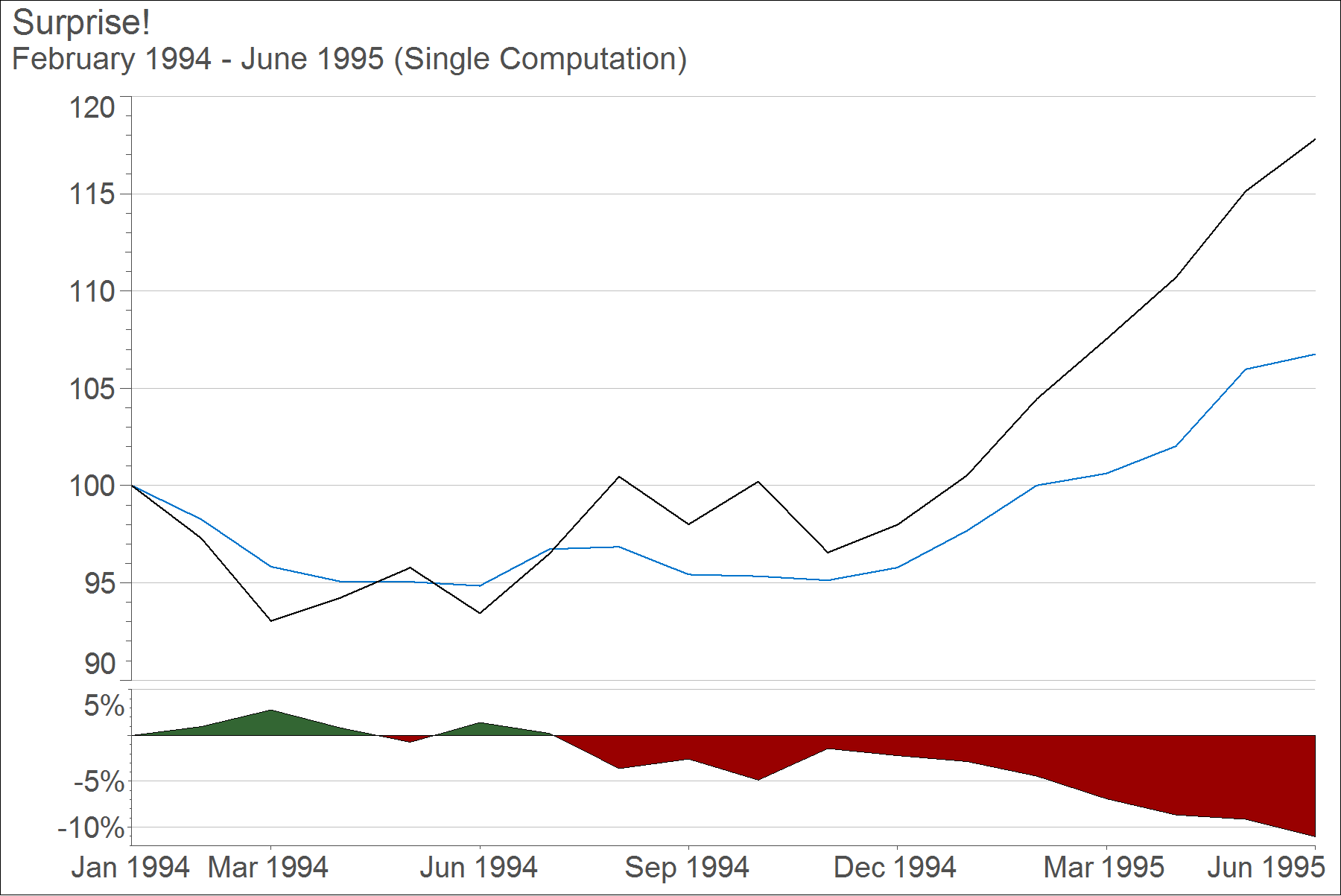

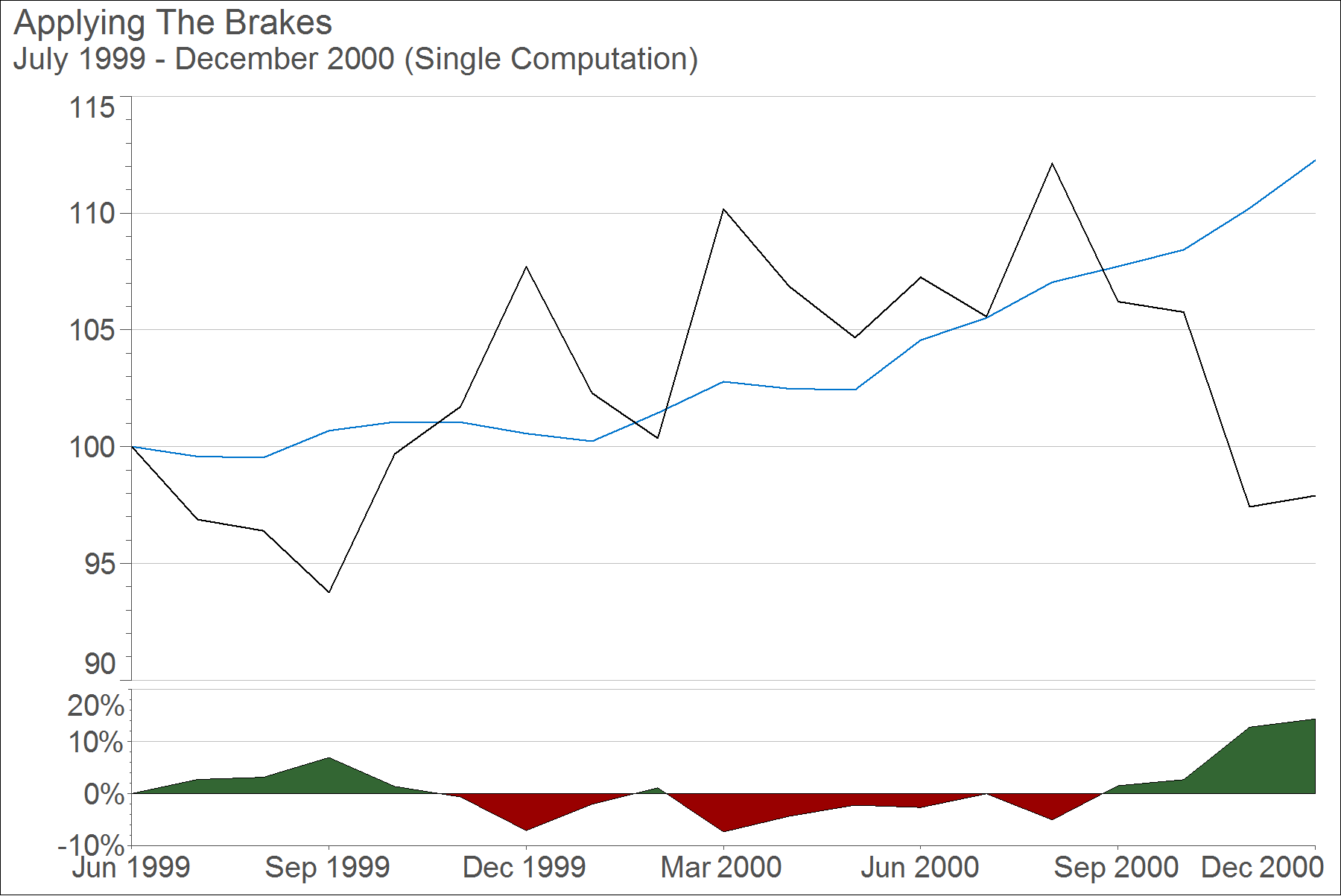

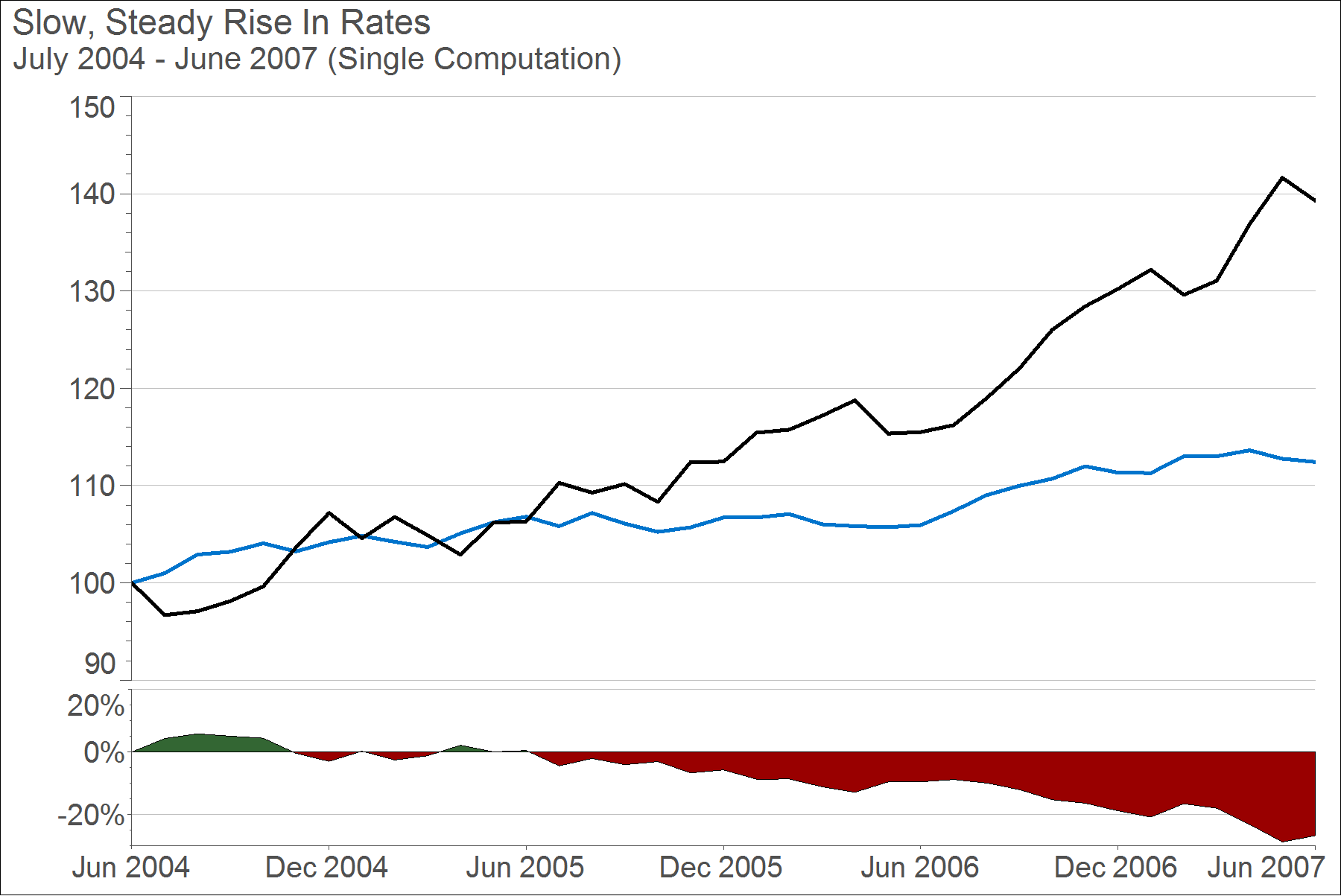

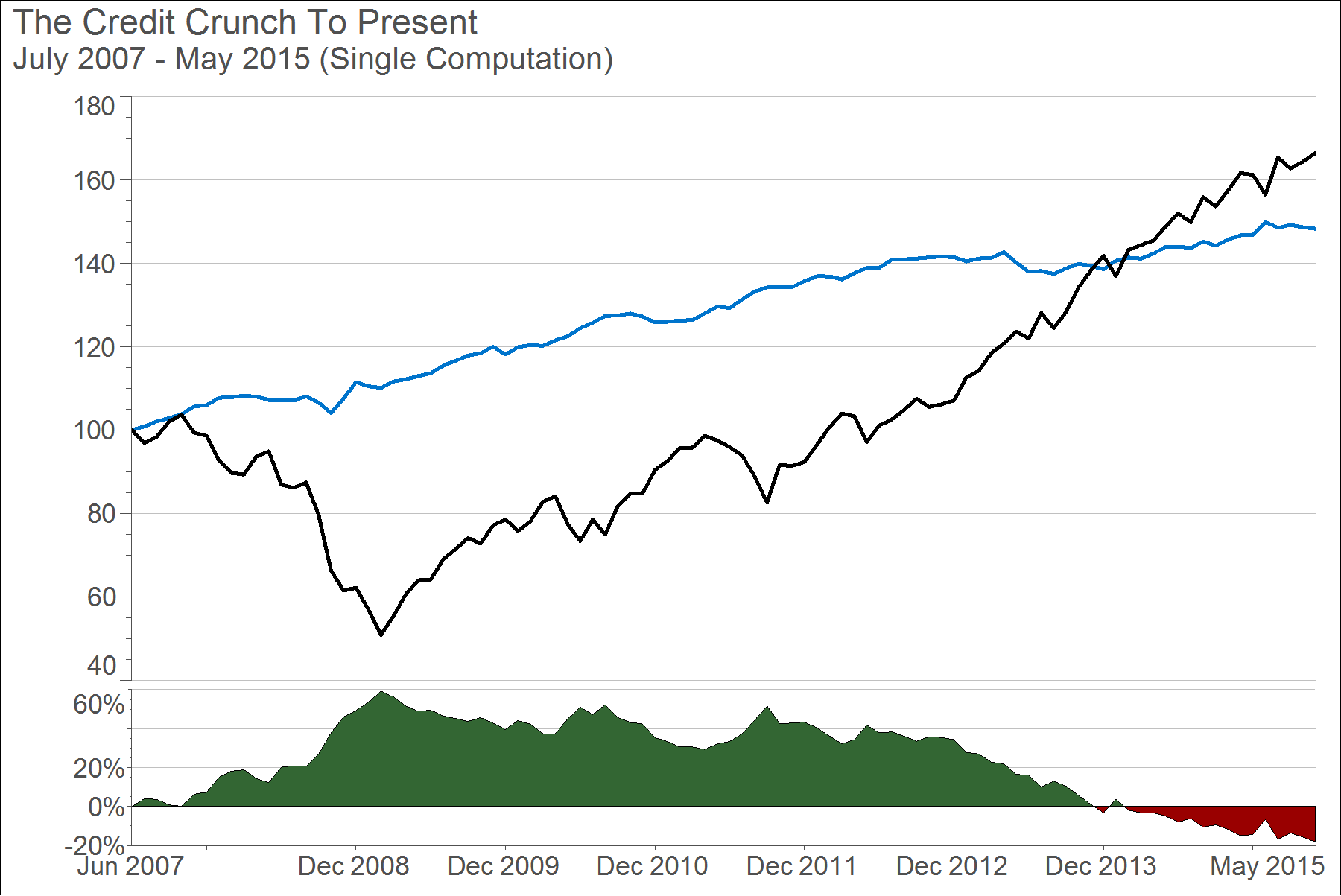

During these periods, the performance of fixed income may surprise you. In the past 20 years, there have been essentially three periods of a rising federal funds rate. Below are three graphs comparing the performance of fixed income (as represented by the Barclay’s US Aggregate) and equities (as represented by the S&P 500) throughout these three periods. The bottoms of these graphs show the excess return of fixed income over equities. Green indicates positive excess return, while red indicates negative excess return.

![]()

Surprise!: Coming out of the 1991 recession the Fed catches fixed income markets by surprise, raising rates quicker and higher than most investors were expecting. Rates rose from 3.25% to upwards of 6.0%.

Applying the Brakes: The Fed raises rates in an attempt to cool an overheating economy driven by the internet bubble. Rates are gradually raised from 4.75% to 6.50% in less than a year.

Slow, Steady Rise in Rates: The Fed gradually unwinds the loose monetary conditions following the dot-com bust and the September 11th attacks from a low of 1.00% in mid-2003 to a peak of 5.25% in mid-2006.

Fixed income had an annualized return of 4.72%, 8.01%, and 3.98% respectively during these periods. These may be somewhat modest returns, but they’re a far cry from the catastrophic scenarios the doom-and-gloomers would have you believe.

Remember, there is always risk of an unforeseen pull back or recession in the marketplace. In such situations, fixed income has continually proved to limit losses. The inevitable rise in rates will impact the fixed income portion of your portfolio, but it will not be detrimental. What can be detrimental is letting the fear of rising rates cause you to abandon fixed income and take on more exposure to equities. Do not leave your client vulnerable to large losses that are unsuitable for their particular tolerance for risk (see above below).

The Credit Crunch To Present: The liquidity crisis resulting from the housing bust prompts the Fed to cut the federal funds rate from 5.25% to new lows.