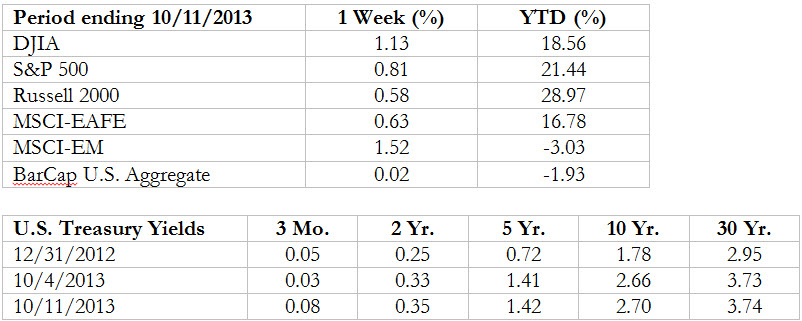

Sadly, the effects of the government shutdown are finally starting to trickle down to our weekly review. Since the federal government is responsible for compiling a fair number of these releases, we have just a few economic data points available for last week.

We would have normally expected results for September retail sales (a closely-watched indicator for domestic commerce), details of the trade deficit, wholesale inventories and the producer price index; unfortunately, none were to be, so we may have a very busy next week or the week after, depending on how long the shutdown lasts. But, as time passes, the data becomes less relevant and is less likely to impact the market. Such is the reality of economic statistics—a lot of effort to compile, then a few minutes of review, and markets price it in and move on to the next piece of news.

Interestingly (since we had the extra space to explore such things), a study put out by the New York Fed recently looked at the timeliness and magnitude of market responses to various economic releases. As might be expected, the most useful information came from data that’s more precise as opposed to vague (and subject to smaller revisions later), more information-packed than not (as in a more direct correlation to forecasting GDP growth, inflation, etc.) or could affect future asset behavior in some way (as opposed to what’s already happened). While there are some general market ‘rules’ that have developed over time for what is ‘good’ news as opposed to ‘bad’ news, much of this data is relative and ever changing. For example, what might be a great jobs number one year might not be celebrated the same way a few years later under different conditions/expectations. The Fed study focused mostly on government releases, but in other work, private releases such as the ISM manufacturing and Chicago PMI surveys also belong on a short list.

How much each of these data points matter in a given week is often relative based on what other crises are happening in the world to take temporary precedence. Some of this is related to the business cycle as well. One example is the effect of higher-than-expected unemployment releases during recessions (taken poorly by markets due to the obvious bad news) versus expansions (when this news is taken a bit better—presumably, since it could delay the need for central bank action to put on the brakes, effectively keeping the party going for longer). Lately, to make things even more complicated, the large impact of central bank quantitative easing on markets has often resulted in ‘good’ news being received badly—especially, if the news is so good it might mean a premature exit from stimulus. This is unusual, however, and a function of the unconventional policies of the past few years.

What data generates the greatest reaction from markets? Generally, monthly nonfarm payrolls, GDP and CPI have been specifically mentioned statistically, although weekly jobless claims are also mentioned in other studies as a more frequent but somewhat important data piece. Negative surprises generally have a larger impact on asset pricing than do positive surprises. Then again, we intuitively already knew that. Perhaps these tendencies may help provide some context as you browse these pieces week to week.

From the few economic data pieces we do have…

(0) The University of Mich. consumer sentiment survey declined from 77.5 in September to 75.2 in the preliminary October release—which was largely similar to the 75.3 expected. Naturally, expectations for the future deteriorated along with confidence about congressional goings on; however, opinions of current conditions edged up a bit. Inflation expectations nudged downward for both the 1-year and 5-year look-ahead projections to just under 3%; administrators assumed this may have something to do with lower gasoline prices. Naturally, this is usually taken with a grain of salt by frequent watchers of that volatile metric.

(-) The NFIB small business optimism index fell a bit from 94.1 in August to 93.9 in September—lower than a forecasted 94.3. Expectations for sales improved, as did plans to increase capex spending—which are both positive signs. However, earnings trends, expectations for the overall economy and hiring plans worsened a bit to offset those factors somewhat. Small business optimism continues to improve and is near a post-crisis high point, but has lagged the pace of the typical business cycle and that of larger firms. Additionally, small business owners have continued to be much more pessimistic about government affairs and gridlock in Congress. This can spiral into a continued reluctance to hire and expand, or at least a delay in doing so, as we’ve noted before. This is another example of how sentiment plays a trickle-down effect in the economy.

(-) Initial jobless claims for the October 5 week jumped by 66k to 374k—the largest weekly increase since the Hurricane Sandy period. What happened? According to the short-staffed Labor Department, continued problems with California’s computer system and layoffs of non-Federal workers due to the government shutdown were roughly equally to blame. The initial claims by Federal workers themselves (who are eligible to collect unemployment while furloughed) will start rolling in next week, so that will affect numbers. Continuing claims for the September 28 week declined by 16k from the prior week to 2,905k, but still surpassed the 2,863k expected. Other than these multiple unique factors, the base claims figure isn’t all bad, but there is so much underlying noise, we’ll need to wait a few weeks for this situation to normalize.

(0) The FOMC minutes for the September meeting didn’t bring any surprises, but did add additional color to the underlying conversation about tapering. There appears to be a broad-based understanding by the committee that tapering has to happen, and an increasing awareness of the reaction to this communication by bond markets—based on what happened this spring/summer.

The Fed continues to have concerns, which is why tapering didn’t happen last month, and may be pushed off to December (base case) or even early 2014. These concerns involve ‘risk management considerations, namely housing, which is a critical component of economic growth and domestic employment (both direct through construction trades and others, as well as peripheral, which includes home improvement stores, carpet manufacturers, furniture, appliances, etc.). Seeing mortgage rates rise a fraction to a full percent is problematic to this market; so, there’s a good chance that when tapering does begin, Treasury purchases may be reduced before MBS are. There is a great deal of conversation within the committee ranks about when tapering should begin, how much it should be and when it should end—with a nod to the fact that the Fed chair will be a new one.

By now, most everyone has heard the news that Janet Yellen is the nominee for the next Fed chair. She was certainly the frontrunner with Larry Summers bowing out of the race. Often these types of announcements can give the market a shot in the arm, but with the debt limit and shutdown overhang, this is the type of thing likely to be pushed off the front page. Markets have been fairly warm to this choice, as she’s seen as likely to continue Bernanke’s current accommodative monetary policies. In several respects, her views seem to be quite similar to those of Bernanke based on past policy comments (something often gauged through speeches Fed members give regularly).

Yellen has been the champion of what’s called the ‘optimal control’ model for interest rate positioning. This refers to several simulations the Fed uses for interest rate policy based on outcomes several years out, even if the path may lead to some less desirable shorter-term results (a nod to the Fed’s sometimes-problematic dual mandate—in the current case, implying employment as a more important policy goal than potential inflation). The implication is that policy is more accommodative than it would otherwise be if not for the need to use unemployment as a key consideration. Overall, her policy record appears a bit more dovish than it does hawkish, with a consistent focus on employment as a decision variable, and feels the current elevated unemployment rate is the result of cyclical rather than structural components. All of these factors point to more Bernanke-like viewpoints and policies looking ahead. However, to temper this apparent dovishness, she seemed to express concern about inflation during the mid-1990’s period while a Fed governor and before serving as chair of Bill Clinton’s Council of Economic Advisers and President of the San Francisco Fed.

She has largely remained behind the scenes—more of an academic and economic researcher than political operator (as was Bernanke before the crisis cast him into a higher profile and household name). Perhaps such anonymity is not a bad thing in a time when politicians are held in quite poor regard.