(-) The third and somewhat final estimate of first quarter GDP was revised downward—and quite dramatically—from the second estimate of 2.4% down to 1.8%. The revision was based entirely on a reduction in consumer services consumption growth, which ended up accounting for essentially the full 0.6% in question (a component that fell from 3.4% growth in last GDP release to only 2.6% in this one).

Although relatively dramatic, measures of growth for previous quarters don’t significantly change how economists view upcoming periods. Second quarter GDP looks to be largely similar to that of the first quarter—likely around or just below the 1.5-2.0% range. The second half of the year holds a bit more promise, as estimates are a bit higher (more like 2.5-3.0%), but the overall year-over-year figure looks not unlike the ‘normal’ conditions for the past 15 years, depicted in the chart below. And, in order for Fed estimates to play out for their ‘taper’ plans, growth might need to surpass 3% for the next several quarters. For 2014, estimates begin to rise above 3% more consistently.

(+) Durable goods orders for May came in slightly better than expected, up +3.6% relative to a consensus +3.0% gain. Removing transports from the equation brought the gain in orders to +0.7%, compared to expectations of a flat report. Consequently, the difference implies a big move in transports—in this case a +50% gain in non-defense aircraft, and more specifically, Boeing orders (a reminder of how fickle and nichy these series can be—when one company’s products are involved). Core shipments rose +1.7% in May, which was partially due to a revision lower for April.

(0) Consumer spending rose +0.3% for May, which was right on target with analyst forecasts. Personal income rose +0.5%, which came in a bit above the expected +0.2% gain. The wages/salaries portion rose three-tenths of a percent, while interest and dividends grew by nearly 2%—raising the final number. By seeing higher income and flat spending, naturally the savings rate rose from 3.0% in April to 3.2% for May. The headline and core PCE price indexes both rose +0.1% in May, both of which were on target with consensus results, and brought the year-over-year increases to +1.0% and +1.1%, respectively. These reiterated muted inflation pressures on par with CPI.

(-) The Chicago PMI came in a bit weaker than anticipated, falling from May’s 58.7 report to 51.6 for June (versus a forecast of 55.0). The details fell accordingly, with forward-looking new orders and production both lower; however, employment improved by a percentage point. This appeared to be the weaker anomaly of the various manufacturing surveys for the month.

(+) The Richmond Fed manufacturing survey improved from -2 in May to +8 in June, besting the median forecast of +2. The underlying components of the index also improved, along with the headline survey number—including shipments, new orders and employment/workweek. Future expectations were mixed, but remained tilted to expansion, as opposed to pessimism. This most recent release continues the trend of better June results in regional Fed surveys and may lay the groundwork for improved broader manufacturing results.

(+) The S&P/Case Shiller home price index rose more than expected for April, up +1.7% versus +1.2% (year-over-year gain is +12%). Additionally, March’s gain was revised upward from 1% to nearly 2%. In April, home prices rose in all 20 cities covered, but were led by nearly 3% gains in San Diego, LA, Minneapolis, San Francisco and Miami.

(-) The FHFA home price index rose +0.7% for April, which lagged the forecasted +1.1% figure by a bit. However, the March figure was revised upward slightly as well. Interestingly, while the index rose +7% over the past twelve months (led by the Pacific and Mountain regions up +15-20%), prices nationally remain nearly 12% below their pre-crisis peak.

(+) New home sales for May rose +2.1%, which outperformed the +1.3% increase expected, and April’s figure was revised up a percentage point to 3.3%. Sales were positive in all regions but the South. The months’ supply of homes moved upward slightly to 4.1 mo., but this remains lower than it was year-end.

(+) May pending home sales gained more ground than expected, rising +6.7% compared to a forecasted +1.0% increase—bringing the year-over-year gain to +12.5%. The Western U.S. was responsible for the bulk of the monthly increase (+16%), with the Midwest just behind (+10%). Gains in the South were more modest, while the Northeast was flat. This is positive news from a forward-looking standpoint, as it has been estimated that over three-quarters of pending home sales end up being finalized into ‘existing’ home sales down the road a few months—so, some fairly strong correlation between the two series.

(+) The June Conference Board consumer confidence survey rose to a new post-Great Recession high of 81.4, relative to an expected 75.1 reading. Respondent assessments of both present conditions and expectations about the future both improved. (Notably, the survey was taken prior to the aftermath of the June Fed meeting—considering how fickle this series can be, a later survey may have colored the results differently.)

(+) The final copy of the University of Michigan consumer sentiment index rose from its preliminary estimate of 82.7 to 84.1 for June—which surpassed expectations of an 83.0 result—and brought the index to a level just below its May post-recession high. Consumer assessments of current conditions and future expectations improved a bit with the revised figure, and inflation expectations also ticked downward—but remained near their historical 3% range.

(+) Initial jobless claims for the June 22 week fell from the previous week’s revised 355k down to 346k (just above expectations of 345k), with no special factors affecting the results. This brought the four-week moving average of claims to an identical 346k. Continuing claims for the June 15 week came in at 2,965k, which were little changed from the prior week and a bit higher than the 2,953k expected. These are now consistently coming in at below the 3,000k range.

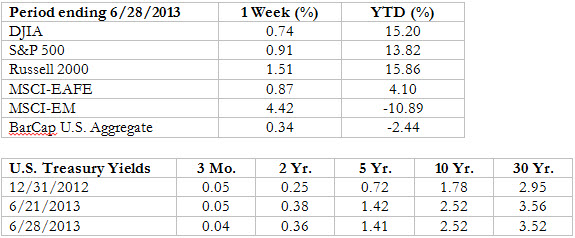

You had to assume the Fed would make an attempt to pull back on the prior week’s poorly-received/misunderstood communication. FOMC members make speeches quite often to groups in their districts, and around the country, and often use these forums to fine-tune Fed views that may need better elaboration. Last week, separate speeches by New York Fed President Dudley and San Francisco Fed President Williams centered around a theme of ‘hold on a minute’—in that current labor and economic growth trends were not robust enough yet to warrant an early exit from QE. In fact, per the comments, there is just as good of a chance of accommodation lasting longer than was implied by earlier Fed comments; and, market expectations for an early exit would be ‘quite out of sync’ with FOMC statements and participant views.

Since the U.S. and global economies continue to experience a significant estimated output gap (difference between current economic output vs. where we could be if firing on all cylinders) and inflation is tempered, the rush to tighten is lessened. Indeed, applying the tightening ‘brakes’ implies lightening up on the QE gas pedal first, and even that doesn’t seem to be in the cards as of yet. Seeing economic and labor conditions improving and returning to some semblance of ‘normal’ is quite different than attempting to handle a fast-paced level of growth on the verge of overheating.